Once a stock is on the up, can you ride on its coat tails to enjoy better returns? Investment research experts Dimensional explore whether chasing momentum fits into a sensible investment strategy.

By Wes Crill, PhD, Head of Investment Strategists and Vice President at Dimensional Fund Advisors

‘Stock price momentum’ generally refers to the tendency of stocks with relatively high prior returns to continue their relative outperformance. Nearly 30 years after its formal discovery, its appeal remains in the eye of the beholder.

Some see its outsize historical premium – 9.1% per year in the US – as validation for investing in momentum-focused strategies. Others point to the extreme turnover and occasional catastrophic outcomes for the premium as insurmountable hurdles.

As with many things in life, the truth is somewhere in between. While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term asset allocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfolio management decisions.

A matter of time

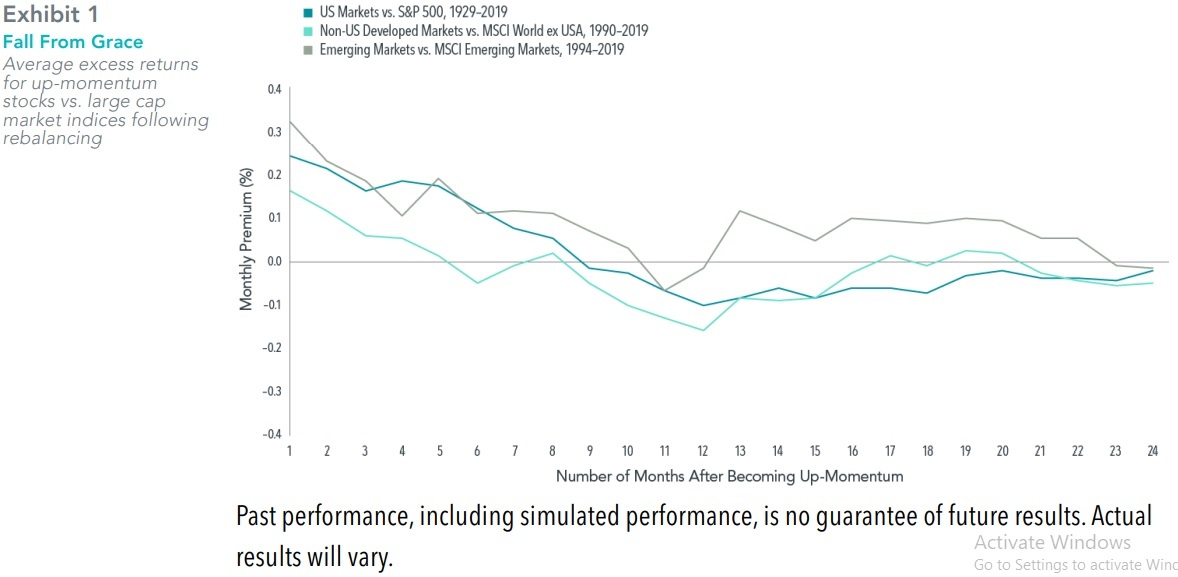

Prior return characteristics contain meaningful information about expected stock returns, but only over short time horizons. In the first month following a sort on past-year return, US up-momentum stocks – those ranking high relative to the market – outperformed the S&P 500 Index by 0.24%.

However, this return advantage tends to decay rapidly: as we see in Exhibit 1*, the excess return for US up-momentum stocks nearly fell by half, to 0.13%, just six months after being classified as up-momentum. By nine months, this was no longer positive. Similar behaviour is observed in non-US market momentum premiums as well.

Rapid decay in the premium implies high turnover to capture it. Since up-momentum stocks typically are no longer contributing to the premium 9–12 months following their prior return ranking, momentum strategies may be likely to hold stocks for less than a year on average. This implies turnover exceeding 100% for a continuous focus on the premium.

Momentum-focused strategies are banking on the sheer size of the premium outweighing the costs of that turnover. Unfortunately, our research indicates that the real-world outcomes for live momentum strategies do not support this outlook.

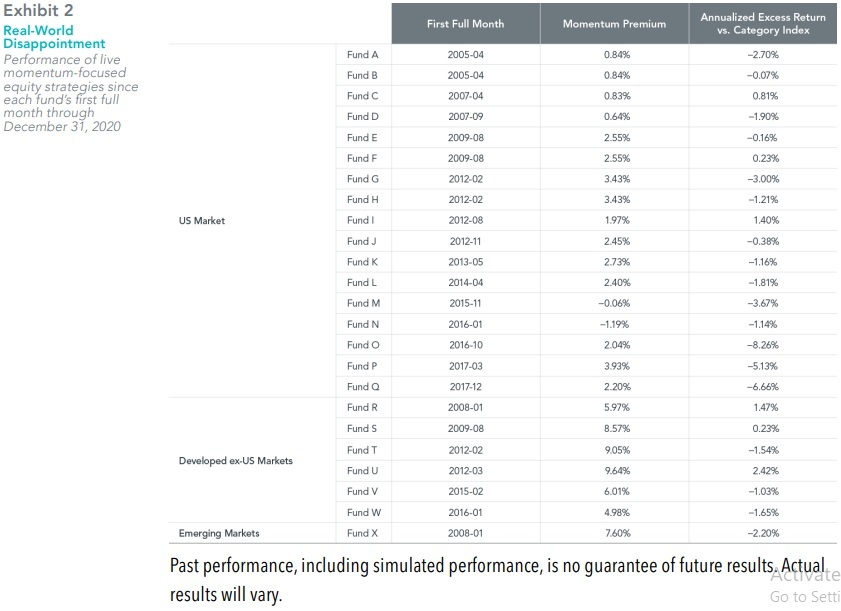

A study of 24 momentum equity funds shows that a majority have underperformed their Morningstar Category Index after fees and expenses despite, in many cases, benefiting from strong realised momentum premiums. For example, as shown in Exhibit 2#, Funds G and H are approaching a decade of live results and have underperformed their category indices by 3.00% and 1.21% per year, respectively, despite an average Fama/French US Momentum Factor return over that time of 3.43%. So anecdotal evidence suggests that momentum-focused funds generally have not helped investors outperform, even during environments when the momentum premium was favourable.

Complement or insult?

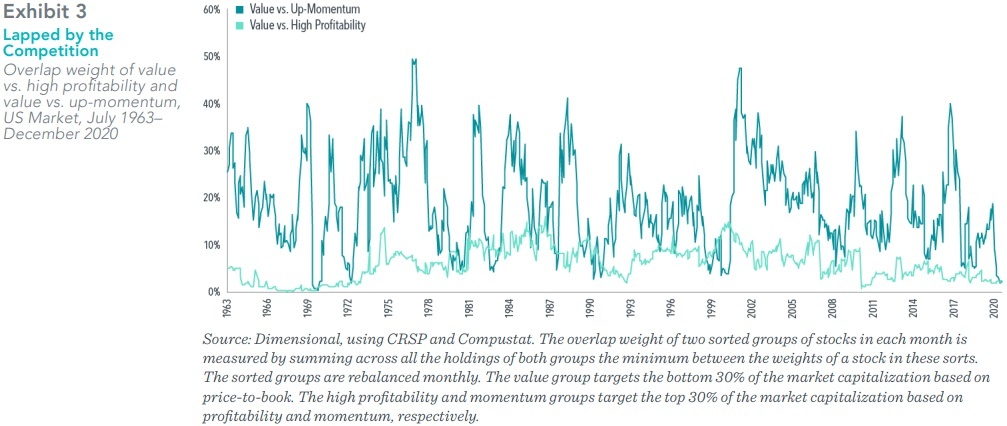

Some investors believe momentum is a good complement to value due to the low historical correlation between the premiums. However, the overlap between momentum and value strategies has fluctuated to an extent that may be inappropriate for such an objective. As shown in Exhibit 3, the percent of market cap in common between value stocks and up momentum stocks has frequently exceeded 30%. Contrast this with high profitability stocks, which have exhibited lower and more stable overlap with value.

Considering the relatively low turnover required to capture profitability premiums, we believe high profitability strategies make a more compelling case as an asset allocation complement to value.

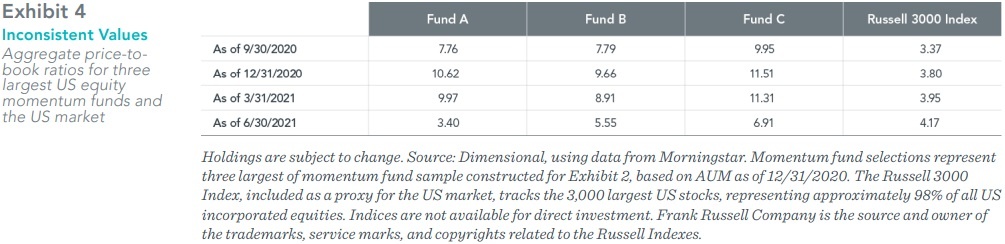

Variability in the overlap between momentum and value may lead to substantial uncertainty in one’s total portfolio exposure to value when momentum is pursued in a standalone strategy. Exhibit 4 shows marked inconsistency in valuation characteristics for the three largest US equity momentum funds during the value premium rally of late

2020 to early 2021. Price-to-book ratios for all three surged briefly in the fourth quarter of 2020 before dropping precipitously during the second quarter of 2021. The largest of the three funds (Fund A), in particular, finished Q2 slightly value-tilted compared to the overall market (Russell 3000 Index).

Love it or leave it

Implementation challenges do not obviate the need to consider momentum when designing and managing portfolios. Rather, they highlight the need for a framework that governs how one can efficiently use different signals about expected returns. One such framework is to categorize variables by the horizon over which they contain information about differences in expected returns.

We believe long-term drivers of returns, such as market capitalisation, relative price, and profitability, are reliable foundations of portfolio structure, as research has shown they are relatively stable variables enabling low turnover, cost-effective portfolio design.

Incorporating additional variables into portfolio asset allocation entails trading off exposure to an existing one. We believe this is an undesirable outcome for a short-term driver of expected returns, such as momentum, because of the increase in expected turnover it will exert.

Fortunately, research shows that we can increase expected returns by considering momentum characteristics among the many inputs when buying and selling stocks. Buy and sell decisions can be made to result in portfolios that favour stocks with upward momentum characteristics. For example, given a set of stocks with equally attractive size, relative price, and profitability characteristics, buys can be delayed on securities that exhibit downward momentum until that effect has dissipated. Conversely, sales can be delayed for securities exhibiting upward momentum.

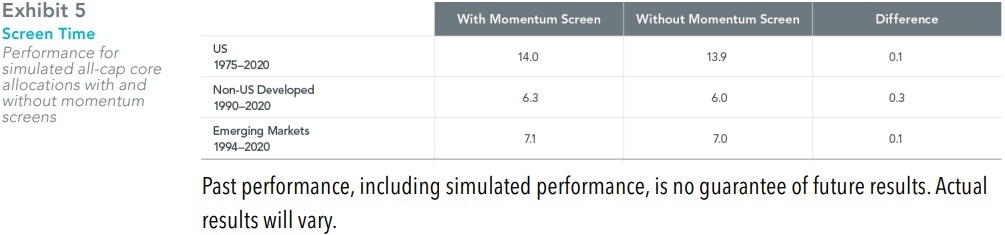

As the all-cap core simulations in Exhibit 5 demonstrate, momentum screens have meaningfully increased the returns of marketwide strategies that overweight smaller, lower relative price, and higher profitability stocks. Of course, one might expect even greater impact for asset class strategies focused on small cap or value stocks, as recent underperformance associated with downward momentum may send stocks disproportionately into low-price segments of the market.

Using momentum this way generally does not increase expected turnover because its application potentially delays buy and sell transactions. This implies a lower opportunity cost than incorporating momentum as a driver of asset allocation. For example, had the momentum premium been flat during the sample period of analysis in Exhibit 5, the net effect on performance would have been zero. Contrast that with how many momentum-focused funds underperformed even with the benefit of positive momentum premiums.

Object in motion

One of the challenges with systematic investing is the uncertainty around premiums. We believe portfolio design must take into account the possibility that targeted premiums do not show up for long periods of time. This is arguably even more important with a premium such as momentum, which requires high turnover to pursue and lacks a consensus story for what drives it. Rigorous research combined with decades of systematic investing expertise help inform portfolio design and management by identifying efficient uses for the many sources of information about expected returns.

This article was from our investment partners, Dimensional Fund Advisors LP.

*Exhibit 1 notes:

Filters were applied to data retroactively and with the benefit of hindsight. Groups of stocks and their returns are hypothetical, are not representative of indices, actual investments or actual strategies managed by Dimensional, and do not reflect costs and fees associated with an actual investment. Indices are not available for direct investment. MSCI data © MSCI 2021, all rights reserved. S&P data © 2021 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved.

In USD. Source: Dimensional, using data from CRSP and Bloomberg. In the US, the up momentum group includes stocks across NYSE, AMEX, and NASDAQ with greater momentum than the top 30% momentum stock within NYSE. Outside the US, the up-momentum group represents the top 30% of the stocks in the large cap universe based on momentum. In the US, large caps include stocks listed on NYSE, AMEX, and NASDAQ with market capitalization greater than the median market capitalization of NYSE-listed stocks. Outside the US, large cap stocks are defined as the top 90% of market capitalization. The monthly returns on the up momentum group are examined relative to the relevant benchmark over the subsequent two years. Momentum is evaluated over the trailing one year, skipping the most recent month. Up-momentum groups are rebalanced monthly. REITs, tracking stocks, and investment companies are excluded from the universe. In addition, to be included in the international analyses, stocks need to meet certain minimum market capitalization and liquidity requirements. Returns of MSCI indices used in this analysis are gross of dividend withholding taxes.

#Exhibit 2 notes:

In USD. Source: Dimensional, using data from Morningstar and Ken French’s website: Kenneth R. French – Data Library (dartmouth.edu). Sample includes funds in the US equity category as of December 31, 2020, with momentum appearing in the name. Multifactor funds that do not primarily focus on momentum and funds with fewer than 36 monthly returns as of December 31, 2020, are excluded. Data for funds with multiple share classes is aggregated at the fund level using the asset weighted average of individual share class observations. Momentum coefficient shows how correlated the fund’s returns were to the momentum premium. Momentum premium is the average return of the Fama/French US Momentum Factor times 12. Annualized return vs. category index is the difference in annualized returns between the fund and the Morningstar category index since the first month of returns for the fund. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

IMPORTANT INFORMATION FOR SIMULATIONS

Simulated strategy returns are based on model performance. The performance was achieved with the retroactive application of a model designed with the benefit of hindsight; it does not represent actual investment performance. Backtested model performance is hypothetical (it does not reflect trading in actual accounts) and is provided for informational purposes only. The securities in the model may differ significantly from those in client accounts. Model performance may not reflect the impact that economic and market factors might have had on the advisor’s decision making if the advisor had been actually managing client money.

The simulated performance is “gross performance,” which includes the reinvestment of dividends and other earnings but does not reflect the deduction of investment advisory fees and other expenses. A client’s investment returns will be reduced by the advisory fees and other expenses that may be incurred in the management of the advisory account. For example, if a 1% annual advisory fee were deducted quarterly and a client’s annual return were 10% (based on quarterly returns of approximately 2.41% each) before deduction of advisory fees, the deduction of advisory fees would result in an annual return of approximately 8.91% due, in part, to the compound effect of such fees. Past performance, including simulated performance, is no guarantee of future results, and there is always the risk that a client may lose money.

The information in this document is provided in good faith without any warranty and is intended for the recipient’s background information only. It does not constitute investment advice, recommendation, or an offer of any services or products for sale and is not intended to provide a sufficient basis on which to make an investment decision. It is the responsibility of any persons wishing to make a purchase to inform themselves of and observe all applicable laws and regulations. Unauthorized copying, reproducing, duplicating, or transmitting of this document are strictly prohibited. Dimensional accepts no responsibility for loss arising from the use of the information contained herein.

“Dimensional” refers to the Dimensional separate but affiliated entities generally, rather than to one particular entity. These entities are Dimensional Fund Advisors LP, Dimensional Fund Advisors Ltd., Dimensional Ireland Limited, DFA Australia Limited, Dimensional Fund

Advisors Canada ULC, Dimensional Fund Advisors Pte. Ltd., Dimensional Japan Ltd., and Dimensional Hong Kong Limited. Dimensional Hong Kong Limited is licensed by the Securities and Futures Commission to conduct Type 1 (dealing in securities) regulated activities only and does not provide asset management services.

Issued by Dimensional Fund Advisors Ltd. (DFAL), 20 Triton Street, Regent’s Place, London, NW1 3BF. DFAL is authorised and regulated by the Financial Conduct Authority (FCA). Information and opinions presented in this material have been obtained or derived from sources believed by DFAL to be reliable, and DFAL has reasonable grounds to believe that all factual information herein is true as at the date of this document.

DFAL issues information and materials in English and may also issue information and materials in certain other languages. The recipient’s continued acceptance of information and materials from DFAL will constitute the recipient’s consent to be provided with such information and materials, where relevant, in more than one language.

Categories: Investments